Four companies just posted the best numbers in their history. The same week, their stocks fell 25 to 43 percent. This is a column about what the market was selling when it clearly wasn't selling the earnings — because held against the panic, the price sheet points somewhere the income statement can't see.

The last column asked whether price had run ahead of the real economy. Exports hit a record while Korean memory collapsed — the physical thing was strong, the stock wasn't, and the gap stayed open. This one starts from the harder version of that question, because this week the gap didn't just stay open. It widened while the best earnings in the industry's history printed on both ends of it.

Samsung's operating profit came in around nineteen times a year ago. Kioxia's rose 92.7%. TSMC's net income jumped 77.4% to a record. Micron's revenue was up 346%. If earnings were the thing the market cared about, this was the week to buy. Instead the four memory names fell together, and only the foundry held.

So the uncomfortable follow-up: if the numbers were records, what exactly got sold?

What goes on the map

Start with the price sheet — that is the part that can be stood behind.

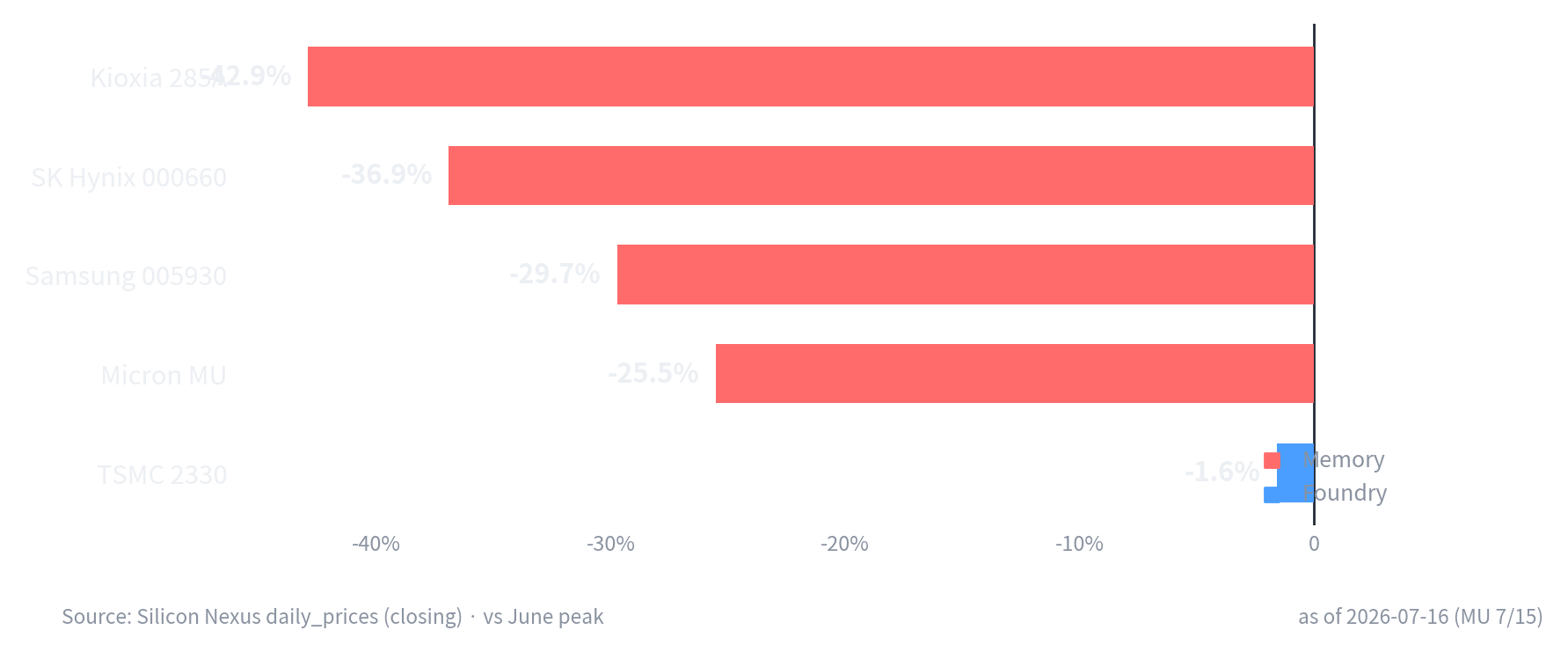

Measured from their June peaks: Kioxia −42.9%, SK Hynix −36.9%, Samsung −29.7%, Micron −25.5%. TSMC — the one foundry in the group — is down 1.6%. Same week, same AI story, and the split is clean: the memory makers cratered, the foundry barely moved. On July 16 alone Samsung fell 8.8%, SK Hynix 11.5%, Kioxia 15.0%, and the KOSPI dropped 6.4% with them. Records at the top of the week, a crash through the middle.

The trigger, in the vocabulary the supply-chain sources actually use, was the cycle — not the capital structure. SK Hynix warned its second quarter could miss consensus by about 8%. Reports circled HBM expansion slowing. China's CXMT climbed to fourth in DRAM, with Samsung testing its chips. NAND oversupply came back into the conversation. None of that touches the earnings that just printed. All of it questions where those earnings sit in the cycle — and that is the thing a record quarter can't answer.

The part quoted from external ledgers

One rule: own data gets shown, external figures get flagged as quotes. The cycle fear above lives in the supply-chain data. The next layer does not — it lives in the US financial press, quoted rather than measured.

That layer asks the same question the column opened with — did price run ahead of the real thing — but in the language of capital structure. It comes in two dialects.

The first is vendor financing. Nvidia invests two billion dollars each into CoreWeave and Nebius and backstops unsold capacity; io-fund points out CoreWeave's capex of $31–35B runs well past its $8.68B of operating cash flow. Money loops through a handful of names. The tell isn't fraud — it's that a company whose demand is supposedly exploding shouldn't need to finance the purchase of its own product.

The second is depreciation. Michael Burry argues hyperscalers write AI hardware off over five to six years when the real replacement cycle is two to three, overstating profits by more than $176 billion across 2026–28. Amazon quietly shortened its server life from six years to five; Meta went the other way. When the same technology gets two opposite accounting choices, the choice is the story.

The historical rhyme is 2001 telecom. Lucent lent customers the money to buy Lucent gear; when demand missed, the loans and the model went down together. The one place the parallel breaks: Lucent was a single strained vendor, and today's buyers are the most cash-rich companies on record. Whether that difference saves them is the verification axis of the next column. (Every figure in this section is external — io-fund, the National Law Review, Burry — flagged as borrowed, not booked.)

The structure that routes around all of it

Here is what the supply-chain data is recording in volume, while the fear above barely registers in it: the move to custom silicon.

A chip a hyperscaler designs for itself never behaves like the ones above. It's consumed in-house, so it never hits a secondary market, never needs vendor financing, and never has to defend a residual value to an auditor. The whole wall those US-lens fears lean on — GPU resale value — simply isn't load-bearing for a captive chip.

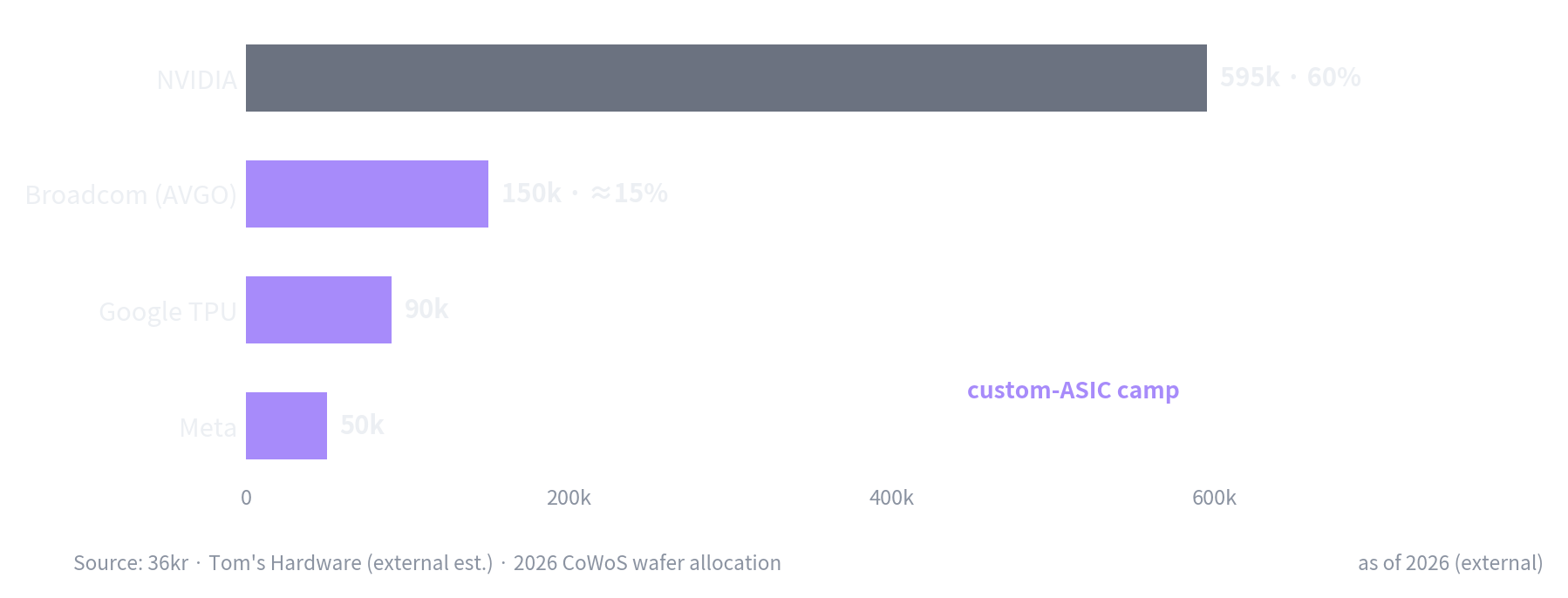

The design sits with Broadcom and Marvell. But a design only becomes a physical chip through one gate: TSMC's CoWoS packaging. So the wafer allocation is the migration's actual speedometer.

Nvidia still owns roughly 595k wafers, about 60%. But Broadcom is at ~150k, Google's TPU at 90k, Meta at 50k — a custom-ASIC camp forming behind the leader as CoWoS capacity itself expands from 65–75k a month toward 120–130k. (Those allocation numbers are external estimates — 36kr, Tom's Hardware — directional only.) The one catch: these chips are captive. The economics of the bypass are open only to the handful of companies large enough to design their own.

Where the five lenses point

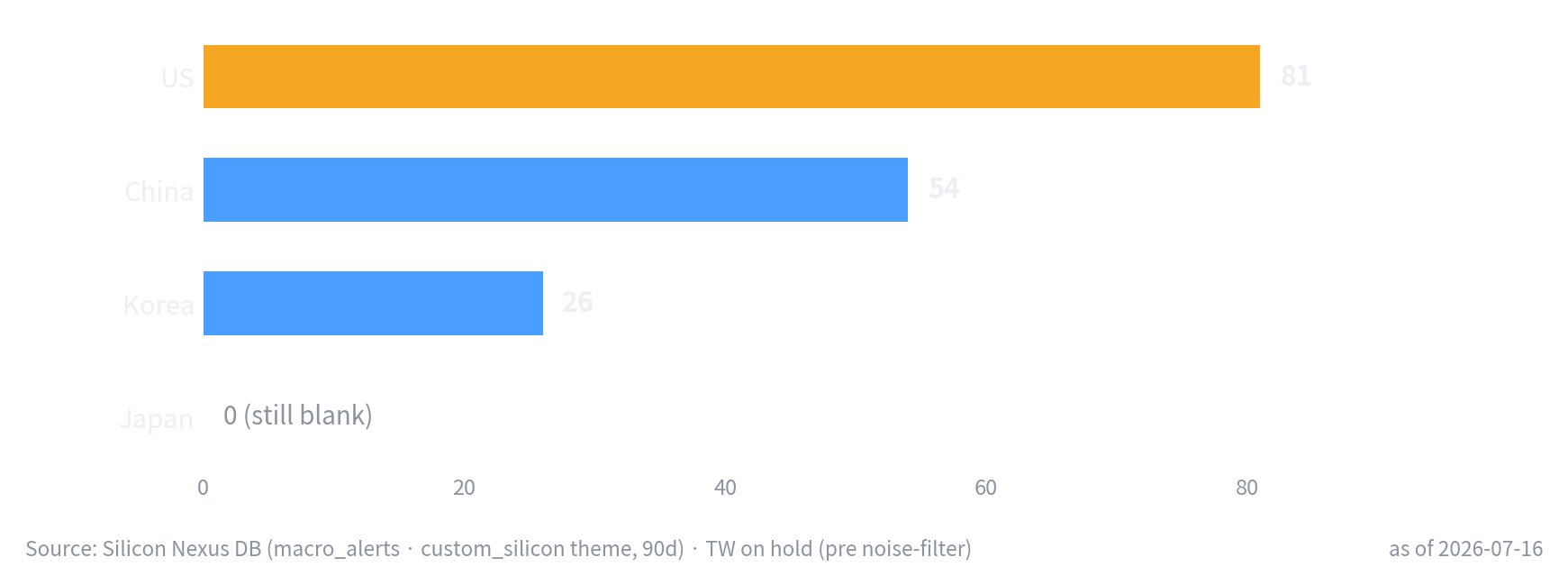

The migration isn't one event. It's five different scenes, each country recording from where it stands. And the count itself is the finding.

The US (81 articles) sees design and capital — Broadcom and Marvell ASICs, hyperscaler in-house chips, and on the flip side the vendor-financing questions. China (54) sees self-sufficiency — Cambricon, CXMT, DeepSeek, a national push off foreign memory. Korea (26) sees dependence — Samsung reviewing the outsourcing of Google's 2nm TPU back-end, both supplier and possible casualty. Taiwan is on hold; its count is polluted by promotional stock posts still to be filtered. And Japan reads zero — which is not absence. Preferred Networks designs its own AI chip; Tokyo Electron and Shin-Etsu enable whoever wins. That is a gap in collection, not a gap in the world, and saying so beats treating the silence as a signal.

Counter-evidence

Three ways this reads wrong. Japan's zero may be a collection hole rather than an absence — it is. The 0–3 hits from querying "vendor financing" in Asian coverage may be a vocabulary mismatch — the same fear shows up there as "HBM slowdown" and "China competition," which is translation, not absence. And the capital-structure fear itself may be overdrawn: H100s still hold 60–83% of their value after eighteen months, and CoreWeave re-contracted expiring capacity at 95% of cost. The wall may be stronger than the bears think.

The landing point is this. Four countries posted peak earnings the same week, and memory fell 25 to 43 percent. What got sold wasn't the income statement — it was the assumption underneath it, GPU residual value, the one thing propping up both the accounting and the financing at once. And the money is already moving: out of the merchant supply chain that carries that wall, into the custom-silicon owners that route around it. This column doesn't predict the next move. It records the one that already happened — the market repricing the durability of the earnings, not the earnings.

The next column tracks whether that repricing sticks: secondary-market GPU prices, depreciation-policy changes, and whether the money keeps flowing to custom silicon or turns back.

Same risk, two languages. The US financial lens calls it vendor financing and residual value — the language of asset prices. The Asian supply-chain lens calls it HBM expansion, cycle peak, China competition — the language of physical supply.

Data: Silicon Nexus dailyprices (closing, as of 2026-07-16) · company IR/filings (Samsung prelim. 7/7, Kioxia securities report, TSMC IR Q2, Micron SEC 8-K) · macroalerts theme counts · external citations (io-fund · NLR · 36kr · Tom's Hardware · Bernstein) to be re-verified before publication. For informational purposes only — not investment advice.

If this analysis was helpful · ☕ Support Us · ✈️ Telegram