The market sold the companies that rent out GPUs as though the rent had already collapsed. In the numbers I actually track, it hasn't — the newest chip hit a new high the day after the crash. This is a column about the gap between what the stocks did and what the price did, written by someone who trusts the price sheet over the panic.

Two columns ago I asked why supply couldn't catch up. One column ago I asked whether, after all that building, anyone would actually show up to fill it — and I came away thinking the buyer list was the part that wasn't slowing.

So this one starts from an uncomfortable follow-up. If demand came, why are the people who built the biggest clusters renting them out — and why did the market sell the renters so hard the moment it heard about it?

What I can put on a map

Start with Colossus. In mid-2026 xAI's flagship site stopped being purely xAI's. Through its parent SpaceX, the company signed Anthropic to roughly $1.25 billion a month for Colossus 1 — about 300 megawatts, on the order of 220,000 GPUs — running to May 2029. Google took a separate slice at about $920 million a month, roughly 110,000 GPUs, from October 2026 into 2029, near $30 billion over the term. Those are the numbers I trust, because they come out of SpaceX's own regulatory filing.

(The other figures floating around — "$30 billion a year," "65–80% margins," "operating costs near 1%" — are not from that filing. They're a 2028 projection from one optimistic blog, and I keep them out of any honest ledger. When I cite Colossus economics, I cite the monthly rent, not the fan fiction.)

The real question isn't the rent. It's why the building's own tenant became a landlord. Colossus 1 was assembled from mixed silicon — Hopper, Blackwell, and older accelerators. When xAI tried to lash it together with newer sites more than ten miles away into a single training cluster, two things bit: latency between distant campuses, and the hardware mix itself. In a synchronized cluster the fast chips wait for the slow ones, so the whole thing runs closer to its oldest part than its newest. Before the lease, reporting put the site's utilization around 11%. So xAI moved its own training onto the uniform-Blackwell sites and rented the mixed one out. The frontier lab couldn't fill its own building, and decided a tenant was worth more than the fix.

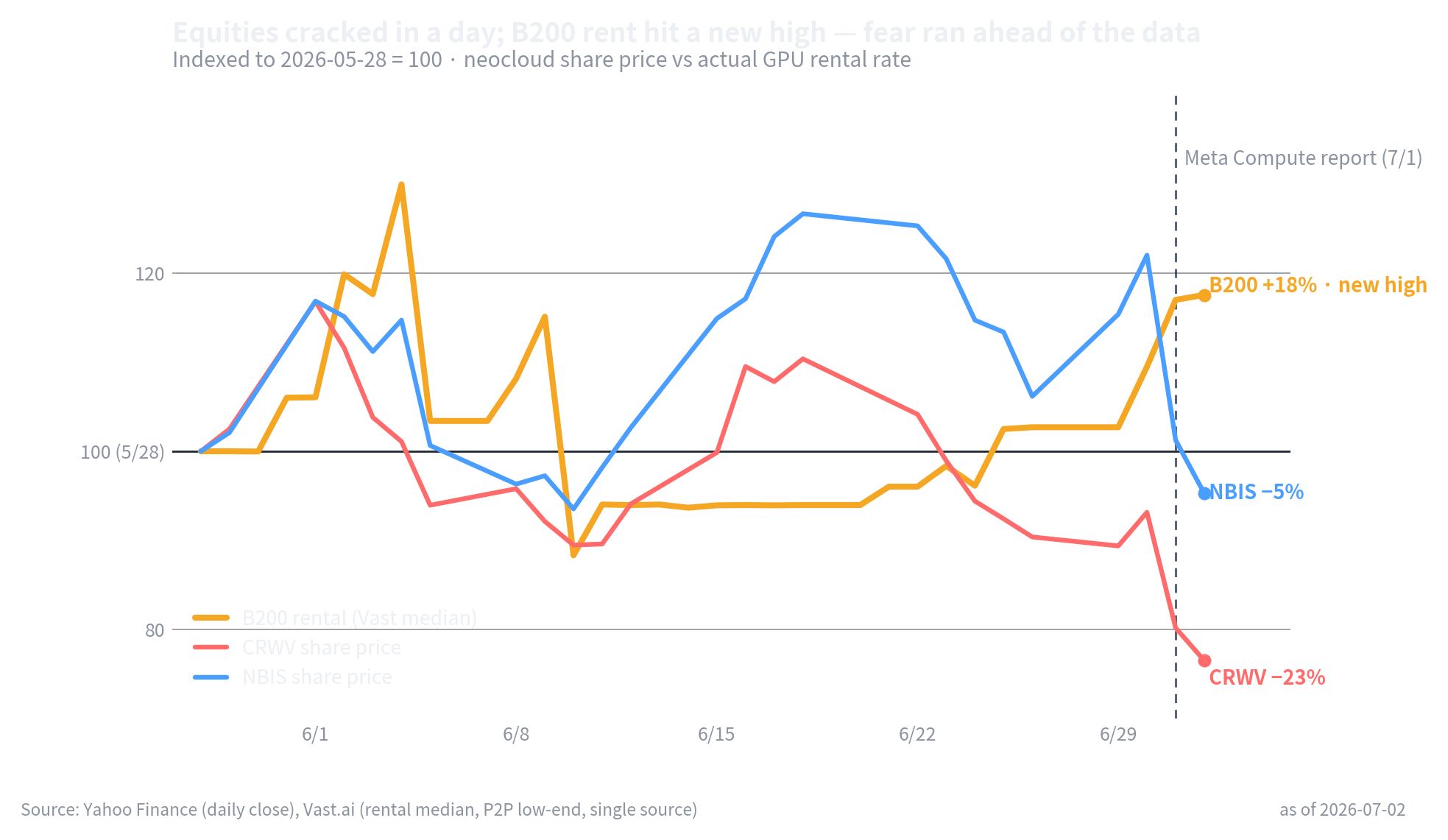

Then Meta made it a category. The reports of a "Meta Compute" effort — leasing idle data-center capacity to outside customers — matter more than Colossus, because Meta is a hyperscaler, not a startup with a spare campus. For years chip valuations rested on one premise: demand always outruns supply. A hyperscaler admitting it has capacity to spare puts a crack in that premise. On July 1 the market read it exactly that way: CoreWeave fell 13.9% to $85.68 on roughly triple its normal volume, Nebius dropped 17.0% to $229.18, and both kept sliding the next day, while Meta itself rose about 10%.

But that sell-off wasn't only about future rent. Meta is one of the biggest customers both firms have — CoreWeave has disclosed about $21 billion of Meta commitments, Nebius up to $27 billion — so the deeper fear was the customer that becomes a competitor, sharpened by a bearish neocloud note from Bernstein the same week. Three fears at once — competition, customer concentration, margins — of which price compression is only one.

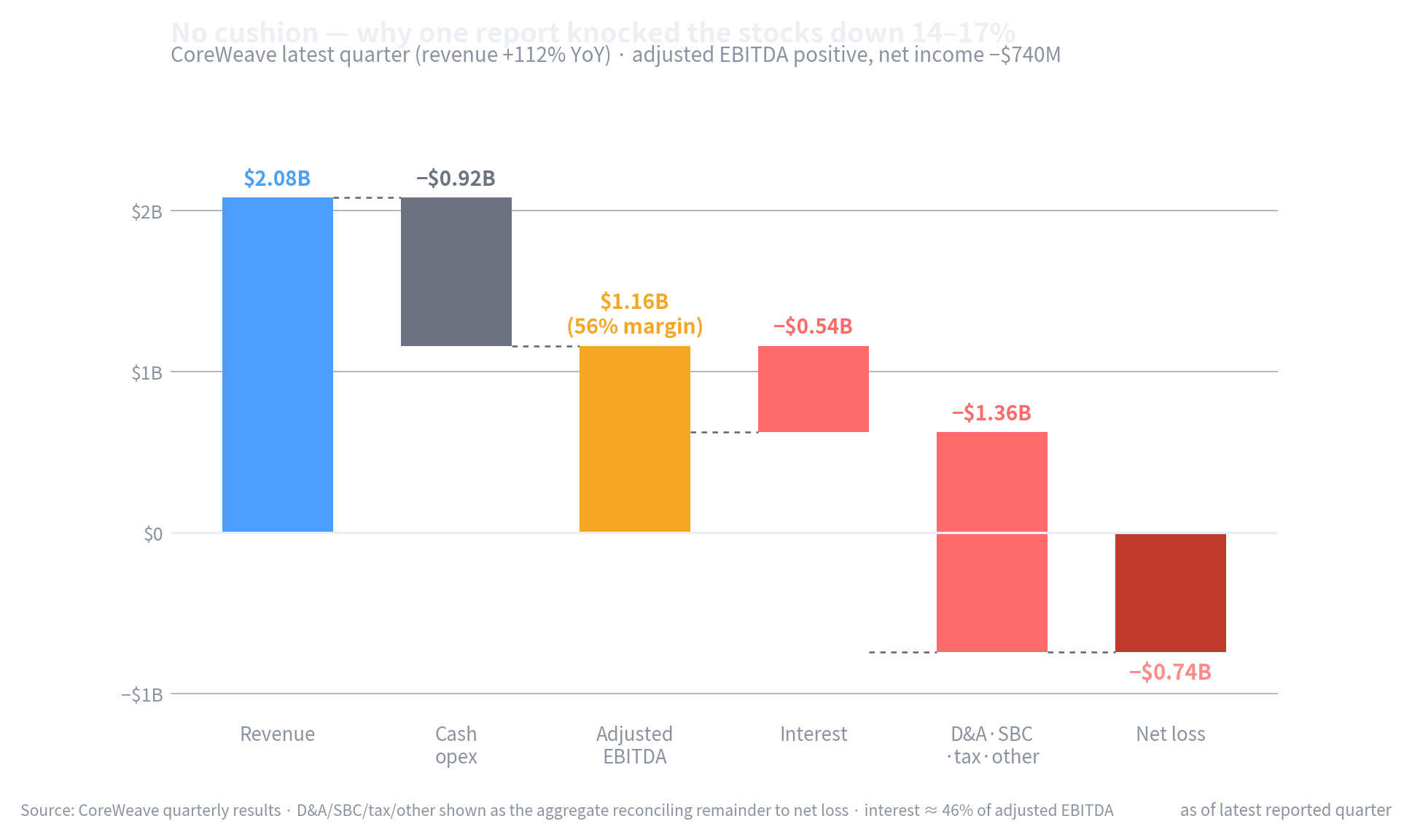

And the landlords are more fragile than their headline margins suggest. CoreWeave's most recent quarter: revenue up 112% to $2.08 billion, and a net loss that widened to $740 million from $315 million a year earlier. Its adjusted EBITDA margin is around 56% — down from 62% a year before — and interest expense alone, about $536 million, eats close to half of that adjusted EBITDA, against roughly $25 billion of debt. Nebius is smaller and growing far faster — revenue up 684% to $399 million — but it too runs a net loss and trades at a steep multiple of sales. The market knows all this, which is why xAI can carry a valuation around $230 billion while CoreWeave, with comparable compute, is worth a fraction of it. Being the landlord is the harder business — squeezed from above by the chip vendor and from below by the cycle.

Figure 3No cushion — why one report knocked the stocks down 14–17%. CoreWeave's 56% adjusted-EBITDA headline is erased by interest and depreciation into a $740M net loss. Source: CoreWeave quarterly results.

That thin cushion is the point. It is why one report could move the stocks double digits in a day — the powder was dry, so a spark of a rumor threw a big flame. But the loss that powder would fuel needs a trigger, and the trigger is a fall in rent. That fall hasn't happened.

Where the map stops and the data starts

Here's where I check the story against my own numbers, because the story wants me to say prices are falling. They aren't — not yet, and not evenly.

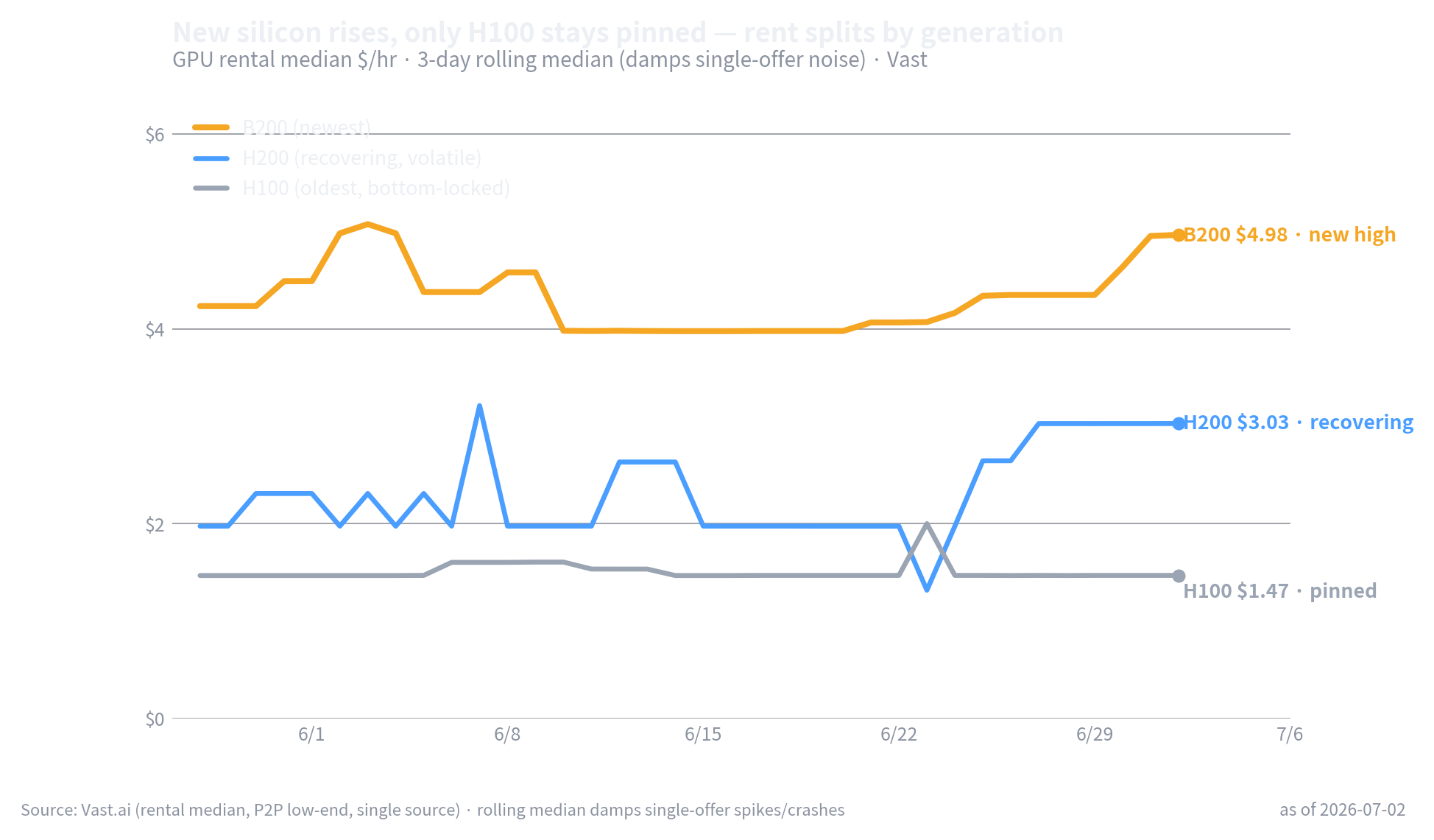

I track marketplace rental rates daily. The caveats first, because they matter: this is Vast.ai, a peer-to-peer market on the cheap end; some days carry only a handful of offers; my clean single-source window is five weeks. This is a floor reading, not the whole market. With that stated, the five weeks say something specific — and they split by generation.

Figure 2New silicon rises, only H100 stays pinned. B200 $4.98 (new high), H200 $3.03 (recovering, volatile), H100 $1.47 (bottom-locked). GPU rental median $/hr, 3-day rolling median. Source:_Vast.ai_.

The H100 — the oldest chip I track — has not moved. Median pinned near $1.47/hr for five weeks. The newest silicon does the opposite: the B200 dipped mid-June toward $3.94 and then climbed back past its old high to about $4.98, and the H200 clawed from under $2 to around $3.03, if unsteadily. A dip that resolves into a new high isn't the signature of oversupply. It's the signature of demand that's still there. Demand is concentrating up the stack; the old generation is lying down.

Which brings me to the gap I can't stop looking at. The equity moved before the price did. On July 1 the stocks priced in a rent collapse — that's what the 14% and 17% were. But the rent itself, in my data, didn't collapse in any generation, and the newest chip hit a new high the very next day, July 2, the day after the crash. The market sold the fear of compression before compression showed up in the thing being sold.

Figure 1Equities cracked in a day; B200 rent hit a new high — fear ran ahead of the data. Indexed to 2026-05-28 = 100. Source: Yahoo Finance (daily close),_Vast.ai_(rental median).

What I'll actually say, and what would change it

Three calls, each one the data will stand behind:

The new-generation rental market is still tight. B200 firm and making new highs; H200 recovering, if unsteady. This lines up with Colossus itself — xAI kept the Blackwell sites and rented the mixed one out. The market isn't letting go of new silicon.

The old generation is bottom-locked. H100 flat at the floor for five weeks, with no rebound in it. I'll go that far and no further: my window doesn't include the decline that presumably put it there, so I can say "stuck at the bottom," not "still falling."

If oversupply comes, it comes to the old generation first. The idle capacity flipping into the rental market — Colossus's mixed chips, a hyperscaler's slack — is mostly old silicon. So the H100 floor is the tripwire. The day $1.47 breaks and keeps going is the day the crack stops being a mechanism and becomes a price. That day is not in my data.

That last sentence is the whole column. The oversupply is real as a structure, and real as a fear the equity already paid for. It is not yet real as a rent. Most of what I read this month collapsed those three into one — "neoclouds crashed, so the glut is here." My own price sheet won't let me sign that. Fear is not a fact. The glut is a thing that could happen, and it would show up first in a number I'm already watching: the oldest chip's floor. Until it breaks, I'm holding the newer read — demand concentrating, not collapsing — and keeping the tripwire in plain sight.

I could be early, or I could be wrong. If the H100 floor gives way and the B200 rolls over, the sequence I just described starts printing, and I'll say so here. If the rent holds and the stocks drift back up, then the market sold a fear it didn't need to. Either way, the honest thing this month is to separate what the equity did from what the price did — and to watch the floor.

There is one wrinkle I have to flag, because it complicates the very tripwire I just named. This week Nvidia began doing something new — underwriting the residual value of the GPUs it sells, in exchange for a share of the buyer's cloud revenue (reported July 2). That is the exact vulnerability the waterfall showed: the depreciation that erases the margin, now offered up to the anchor vendor to absorb. It could be a cushion for the neocloud's soft spot. It could be noise that muddies the signal I'm watching. It could be risk condensing onto one balance sheet. I don't know which yet — but whatever it is, a vendor stepping in to guarantee residual value is itself a sign that residual value, the old-gen floor, is under enough pressure to need guaranteeing. And it means my flat H100 floor may no longer be a clean demand reading; it may be, in part, a defended number. Telling demand from defense is now part of the job. This move has a precedent, and the precedent did not end quietly — vendor lending that peaked after the market had already cracked, and detonated on the lender's own balance sheet. That's the next column.

Data note: rental figures are_Vast.ai_marketplace medians ($/GPU-hr), 2026-05-28 to 07-02, single-source, P2P low end, thin offers on some days. Equity closes from Yahoo Finance. Contract figures from SpaceX's regulatory filing; profitability figures from company quarterly reports; residual-value reporting from DatacenterDynamics (July 2).

A column, not investment advice — and not a solicitation to buy or sell anything.