Built It. Will They Come? — Opinion | Silicon Nexus

✍ Opinion· Jun 20, 2026· Silicon Nexus J.H.· human_opinion

Built It. Will They Come?

Last column I asked why supply can't catch up. This one asks the scarier question on the other side: build all of it, and does anyone actually show up? Part of the answer I can put on a map — 28 gigawatts under construction in the US alone. Part of it I'm guessing at. A column about a buyer list that got longer, written by someone still sorting measurement from hope.

In the last column, I asked why the shortage won't quit even though everyone is building. Record capex, profits everywhere, fabs going up — and prices still climbing. The supply side, I argued, isn't closing the loop the way the textbook promises.

But there's a question hiding on the other side of that one, and it's the scarier of the two. Every argument about a shortage quietly assumes the demand stays. Build the capacity, and someone shows up to fill it. That assumption is doing a lot of work — and historically, it's the one that breaks first.

Here's the memory cycle's oldest trap. A shortage convinces everyone demand is permanent. Capex floods in at the top. The capacity lands a year or two later — right as demand turns out to have been a spike, not a plateau. Supply overshoots into a market that already cooled. Glut. The collapse doesn't come from building too little; it comes from building for a demand that wasn't there. If you wanted to write the bear case for 2027, that's the whole script: the capex in my last column is the setup, and the punchline is an empty warehouse.

So before I get comfortable with "the shortage will persist," I have to take the bear case seriously and ask the unglamorous question: who, exactly, is going to absorb all of this — and is it enough?

Same rule as always. Where I have a number, I'll show it. Where I'm reading tea leaves, I'll say so. What follows splits in two: a part I can put on a map, and a part where I start guessing.

The first half surprised me. I went in expecting to write about whether demand was enough. I came out thinking the demand side might be the part of this story that isn't slowing down at all — and that the buyer list got longer in a way the glut script doesn't account for.

What I can put on a map

So I started where I could actually count something: the United States.

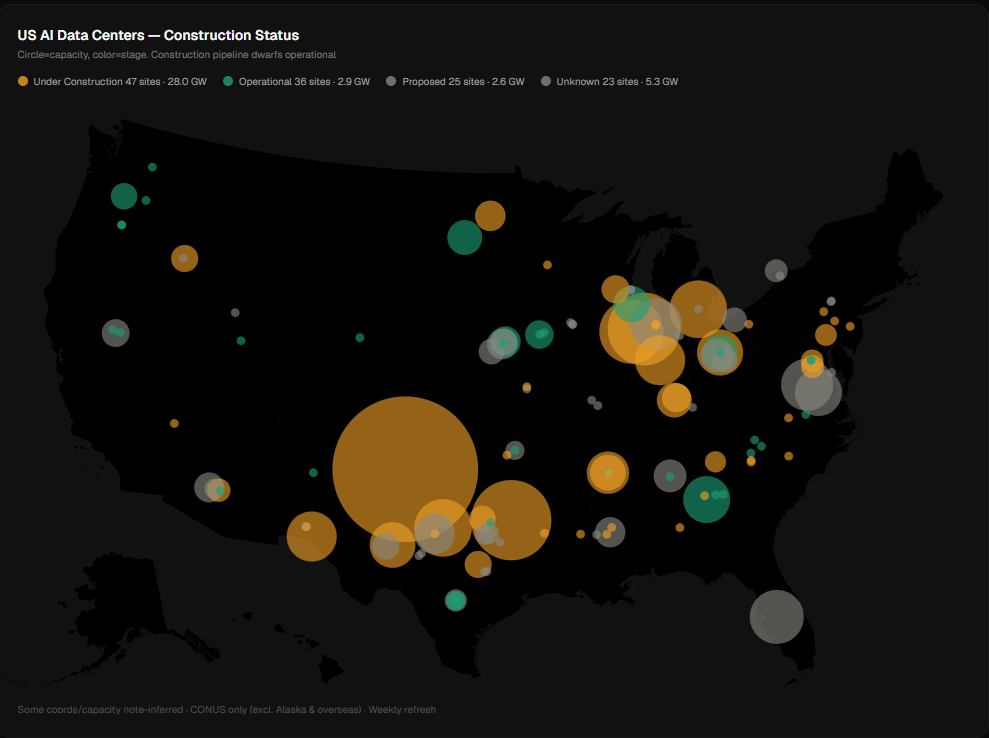

If demand for all this memory and compute is real, it has to show up as physical buildout — data centers, with megawatts attached, that someone is paying to construct right now. Not press releases. Not 2030 targets. Steel in the ground. That's a number I can pull, geocode, and map, so I did.

Each dot is an AI data center; size is its power draw, color its stage. The amber ones — under construction today — come to roughly 28 gigawatts. The ones already operational come to about 3. We are building nine times more capacity than is currently running.

Sit with that ratio, because it's the opposite of a demand worry. Nobody pours concrete on 28 gigawatts of data center because they're nervous about whether anyone will show up. This is the demand side voting with the most expensive ballot there is — poured foundations, signed power contracts, multi-year builds that don't pay back unless the chips inside them stay busy. The buyers aren't hedging.

And the single largest thing on that map isn't who you'd guess. The biggest dot — an 11-gigawatt campus in Texas — isn't Google or Meta or Amazon. It's Fermi, an independent developer most people have never heard of. When the largest single bet on the board comes from outside Big Tech, the appetite has spilled past the usual five names. It's not five hyperscalers carefully sizing their needs anymore. It's a land grab.

This is the part I'm most confident about, because it's the part I didn't have to interpret. The megawatts are permitted. The construction is real. Whatever else is uncertain in this column, the American buildout is not a forecast — it's a measurement.

Where the buyer changes

Now I cross a line, and I want to be honest about crossing it.

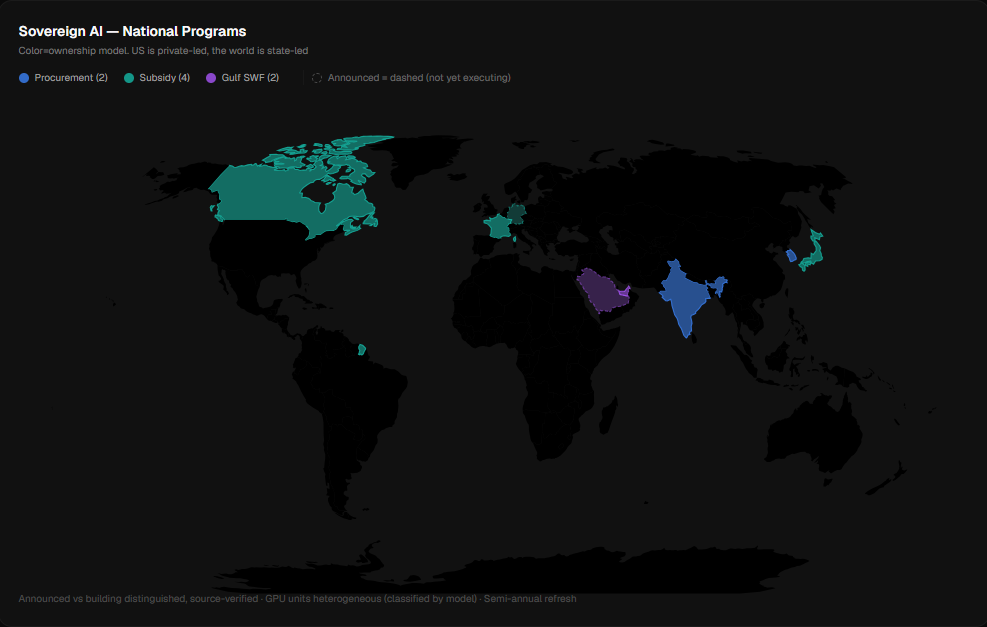

Everything above was American, and everything above was measured. The moment I look outside the US, the ground gets softer. I'm no longer counting poured foundations — I'm reading government announcements, and governments announce things they don't always build. So treat this section the way I treat it: the direction is real, the magnitudes are promises.

Here's the direction. Outside the US, the entity buying the chips increasingly isn't a company. It's a country.

I verified eight national programs against primary sources — government budgets, official announcements, central-bank dashboards, not press recaps. They sort into three plays: the Gulf model, sovereign wealth funding the buildout with the state as first customer; the procurement model, governments buying GPUs directly on a published timeline; the subsidy model, public money seeding fabs and compute. Three routes, one destination — each ends with a government placing an order that used to come only from Silicon Valley.

Now, the obvious objection. The amounts these governments announce dwarf what's actually arrived — Saudi Arabia talks about 600,000 GPUs and has taken delivery of maybe 18,000. If you're hunting for the demand, the loading docks look almost empty.

I'd argue the gap means the opposite of what it looks like. The 18,000 isn't the demand. The 600,000 is. The shortfall isn't proof the demand is fake — it's proof it hasn't been ordered yet. Hyperscalers are already pouring concrete on 28 gigawatts. The national programs are a second wave that has barely begun to place its orders. When you're worried about a glut, the unsettling part isn't the capacity being built — it's that, outside the US, the buyer list is still mostly a queue.

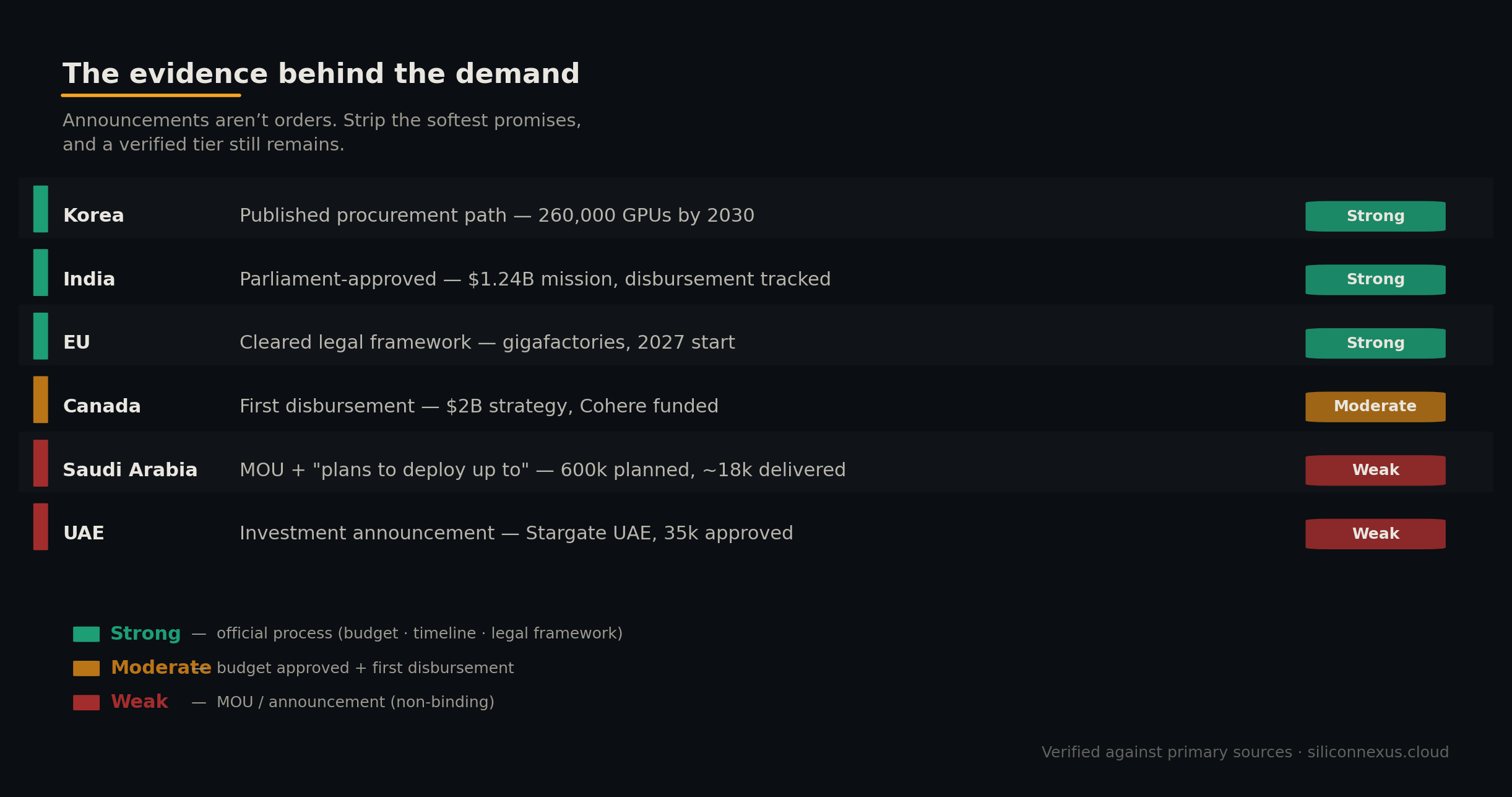

Though not every name in that queue is equally solid, and I won't pretend otherwise. Here's the same eight, sorted by how much I trust the commitment behind each.

Some are scheduled orders — budgets approved, timelines published, legal frameworks cleared. Others are just intent that could still evaporate, and I'm not going to lean on those. But that's the point: even if you delete every soft promise on that chart and keep only the verified ones, a second tier of demand still exists that wasn't on the board two years ago. Governments are buying compute the way they once bought refineries and power grids — something a serious country has to own. They don't replace the hyperscalers. They queue up behind them.

And that changes the shape of the glut question.

What I think it means

Everything past this point is me reasoning, not me counting — weigh it as interpretation.

I don't want to wave the glut script away, because it's a good theory: capacity floods in, demand turns out to be a spike, supply overshoots an empty room, prices crater. It has happened in memory before. The reason I don't think it's the 2027 story is that the buyer side quietly got a second term added to it — and the glut math was written before that term existed.

The bear case runs on one demand source: hyperscalers sizing capacity against their own forecasts, who can pause capex the moment the numbers wobble. But there are two engines now. The second — national programs treating compute as strategic infrastructure — doesn't behave like the first. A government that has decided sovereign AI is a security requirement is far less price-sensitive and far slower to flinch; it's buying for a reason that never shows up on a demand-forecast spreadsheet. Add a buyer like that, and the odds of supply overshooting everyone at once get narrower.

There's a second floor under the demand, too: efficiency feeds this market instead of shrinking it. Every time inference gets cheaper per token, we don't bank the savings — we spend them on longer context, more reasoning, agents that run continuously. That's Jevons' paradox, and it's the answer to my last column's puzzle. Everyone's building and it's still short because the cost of intelligence keeps falling and demand more than fills the room that opens up. Part 6 asked why supply can't catch up; the answer is that the demand side just doubled its engines while efficiency widened the floor under both.

The honest caveat, since this is the part I'm guessing at: this buildout is four or five years old and hasn't been tested by a real recession. Sovereign budgets can be cut; strategic priorities get rewritten when money gets tight. If I'm wrong, it's here — the second engine is younger than the first, and I'm reading a buyer that has mostly announced, not yet paid. But within the data I can actually see, demand isn't the weak leg of this story. It's the part that keeps surprising me upward.

Where this lands in silicon

I write about the supply chain, so let me bring it back there. A second tier of buyers doesn't change what gets bought — it changes how long the order book stays full. The bottleneck names don't move: HBM, advanced packaging, the handful of tools that gate leading-edge capacity. They just get a longer queue standing behind them.

You can see it in who the sovereign programs route through. France's flagship runs on Mistral, and the largest shareholder in Mistral is ASML — the one company without which none of the leading-edge buildout happens, sovereign or otherwise. Every national program, whatever flag it flies, eventually places its order into the same four-country chain: Dutch lithography, Japanese materials and tools, Taiwanese foundry, Korean memory. The buyer list got longer. The list of people who can actually fill it did not.

That's the part I keep coming back to. The demand side added an engine; the supply side still routes through the same narrow set of chokepoints I've been mapping all along. A longer queue against an unchanged bottleneck is, mechanically, a recipe for the shortage to persist — not forever, but longer than a one-cycle glut model would predict.

There's a catch I've left out of this whole column, though, and it's a big one. I've written about demand as if it only has to want the chips. It also has to be allowed to buy them, and it has to find somewhere to plug them in. Both are turning into walls — export controls deciding who gets the compute, local opposition deciding where it's physically allowed to exist. That's the friction sitting on top of everything I just argued, and it's where Part 8 goes.

For now, the thing I'm most confident saying is the narrow thing: I went looking for whether the demand was enough, and came away thinking the demand side is the part of this story that isn't slowing down. The buildout in my last column was real. So, it turns out, is the line of buyers forming to absorb it.

This is opinion, not investment advice — and explicitly the opinion of a developer who follows this market, not a financial professional. Where I've used figures, they're from primary filings and trade statistics, fact-checked as of writing; where I've reasoned past the data, I've tried to say so. The interpretation, and whatever corrections come later, are mine.