Everyone's Building. Why Is It Still Short? — Opinion | Silicon Nexus

✍ Opinion· Jun 15, 2026· Silicon Nexus J.H.· human_opinion

Everyone's Building. Why Is It Still Short?

The textbook says the memory cycle fixes itself: shortage lifts prices, profits fund new fabs, supply floods back, prices fall. The first three steps are happening right now — capex just hit a record. The fourth isn't. This is a column about why the loop's last link looks broken, written by someone who isn't sure yet.

A quick word on what this column is, because it matters for how you should read it.

I'm a developer, not a financial analyst. I built this site because I love watching the chip market, and I write these columns to think out loud — with data where I have it, and with my own read where I don't. When I'm leaning on a number, I'll show you the number. When I'm guessing, I'll tell you I'm guessing. The AI buildout is only four or five years old, so a lot of what looks obvious today is provisional. I'd rather be openly unsure and corrected later than falsely confident now. That's the whole project: thinking that gets revised as the data comes in.

With that said — here's the puzzle.

The loop that's supposed to fix everything

The memory business has a rhythm everyone in it can recite. A shortage pushes prices up. High prices send maker profits through the roof. Those profits get plowed into new capacity. The new capacity floods the market a year or two later. Supply overshoots, prices collapse, and the cycle turns over. Boom, glut, cut, recovery — a loop that has closed itself, painfully, for decades.

So the natural assumption is that today's AI-driven shortage will close the same way. Prices are up, profits are enormous, and the makers will build their way out of it. Give it time.

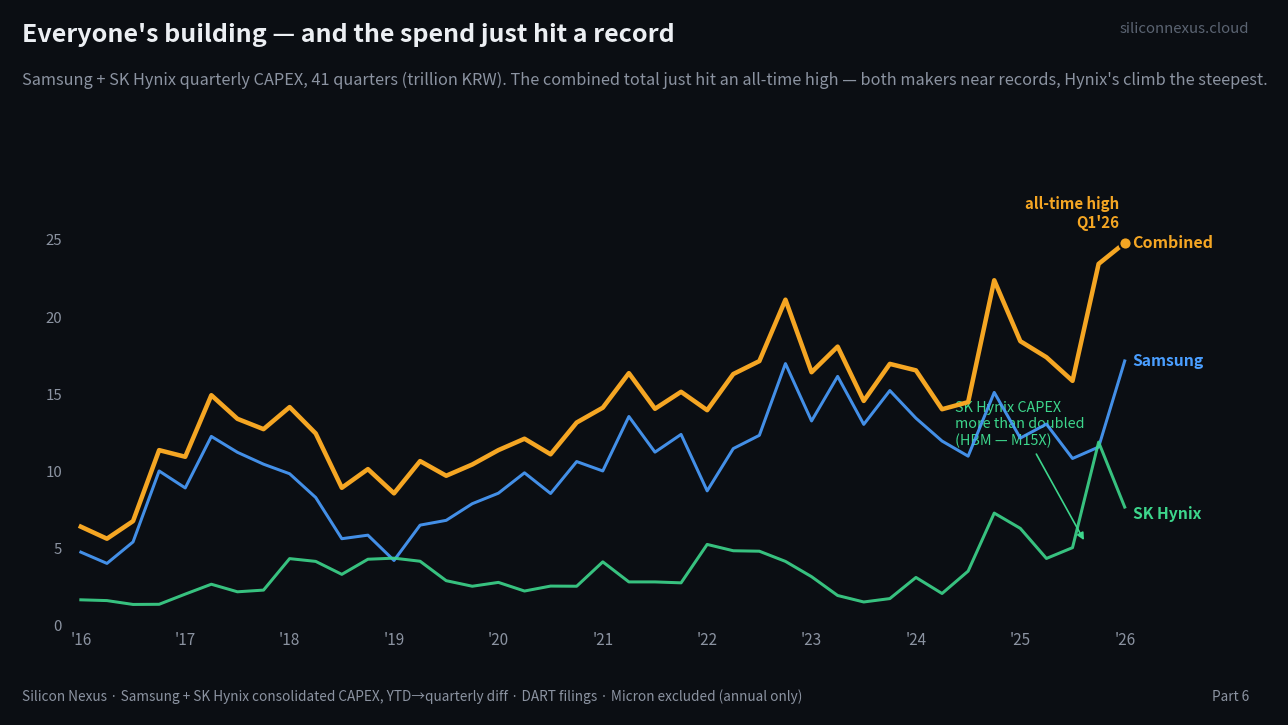

The first part of that is unambiguously true, and you can see it.

That's Samsung and SK Hynix's combined quarterly capital spending over ten years. It's at an all-time high — the two-maker total has never been larger, with SK Hynix's spend more than doubling off the back of HBM. Micron isn't in the picture (it only files annually), but its guidance points the same way: up sharply. The makers are not sitting on their profits. They are building, hard, exactly as the loop says they should.

So supply should be flooding back. Prices should be cooling. And they aren't — DRAM and NAND contract prices are still climbing into 2026. The loop is running, the money is moving, and the relief isn't coming. Why?

Where I stop having clean data — and start reasoning

Here I have to be honest about the seam in this argument. I can show you the capex with hard numbers. I cannot show you, from public data, the thing that would close the loop: bit supply — the actual number of memory bits shipped. That figure lives in paid industry reports and company guidance, not in filings I can pull and verify. So from here on, I'm reasoning from industry estimates and my own read, not from a clean series I built myself. Treat it accordingly.

With that caveat, here's what I think is happening — three reasons the record spend isn't turning into supply.

The capex is being eaten by HBM. The high-bandwidth memory that AI accelerators need is made on the same DRAM lines as ordinary memory — in the makers' own fabs, not at TSMC (TSMC's piece is the logic and the CoWoS packaging, a separate chokepoint for another column). The catch is that HBM consumes far more wafer area per usable bit than commodity DRAM. So a maker can raise capex, convert lines to HBM, book record investment — and still ship fewer ordinary bits than the spending would suggest. The money goes in; the bit count doesn't come out the other side at the same rate. Industry trackers put HBM at roughly a quarter of DRAM wafer demand now, up from far less two years ago. That's capacity that looks like growth on a spending chart but doesn't loosen the commodity market.

The new fabs aren't online yet. Samsung's P5, SK Hynix's M15X, Micron's new US fab — the megaprojects meant to actually add capacity don't reach volume production until 2027 and 2028. The capex is being spent now; the wafers arrive years later. Today's record spending is a bet on demand two and three years out, not a fix for this year's shortage.

Some supply is being withheld on purpose. Burned by the 2023 downturn, makers have been disciplined — NAND capacity in particular is being held back rather than expanded, because flooding the market is exactly the mistake that crushed them last cycle.

Put those together and the loop's last link — new spending becomes new supply — doesn't connect the way the textbook promises. The makers are doing their part. The supply just isn't following on schedule.

And now a wall that money doesn't climb

There's one more piece, and it's the one I find most interesting, because it's new — it isn't a memory-cycle problem at all.

For this whole story to matter, the chips have to go somewhere: into data centers. And data centers have started running into a wall that capital can't simply push through. In April, Maine became the first US state to pass a moratorium on new large data centers, pausing approvals for facilities drawing over 20 megawatts. It isn't a one-off — eleven states are weighing similar limits, and by one bipartisan tally, local opposition across the country has already blocked or delayed more than sixty billion dollars of data-center projects in about a year. The driver is electricity: these sites devour power, local rates spike, residents push back.

To be precise about it, since it's easy to get wrong: this is local and state resistance, not a federal ban — the federal posture has actually been to help, with the administration leaning on big tech over power costs rather than blocking builds. But the direction is what strikes me. For two years the AI story has been about capital — who can spend the most. This is the first chapter where the binding constraint isn't money. You can have the budget, the chips, and the contracts, and still not get the permit. The fight is shifting from the balance sheet to the power grid and the zoning board.

I can't measure that yet — there's no clean series for "permits denied" — so file this under things I'm watching, not things I've proven. But the shape of it feels like a turn.

The question I can't answer yet — so I'm timestamping it

If the loop's last link is genuinely broken, the shortage runs longer than the textbook would predict. And if it runs longer, the interesting question becomes how the makers fund the building — because the record capex is increasingly running ahead of the cash coming in, which is the thread Part 4 pulled on.

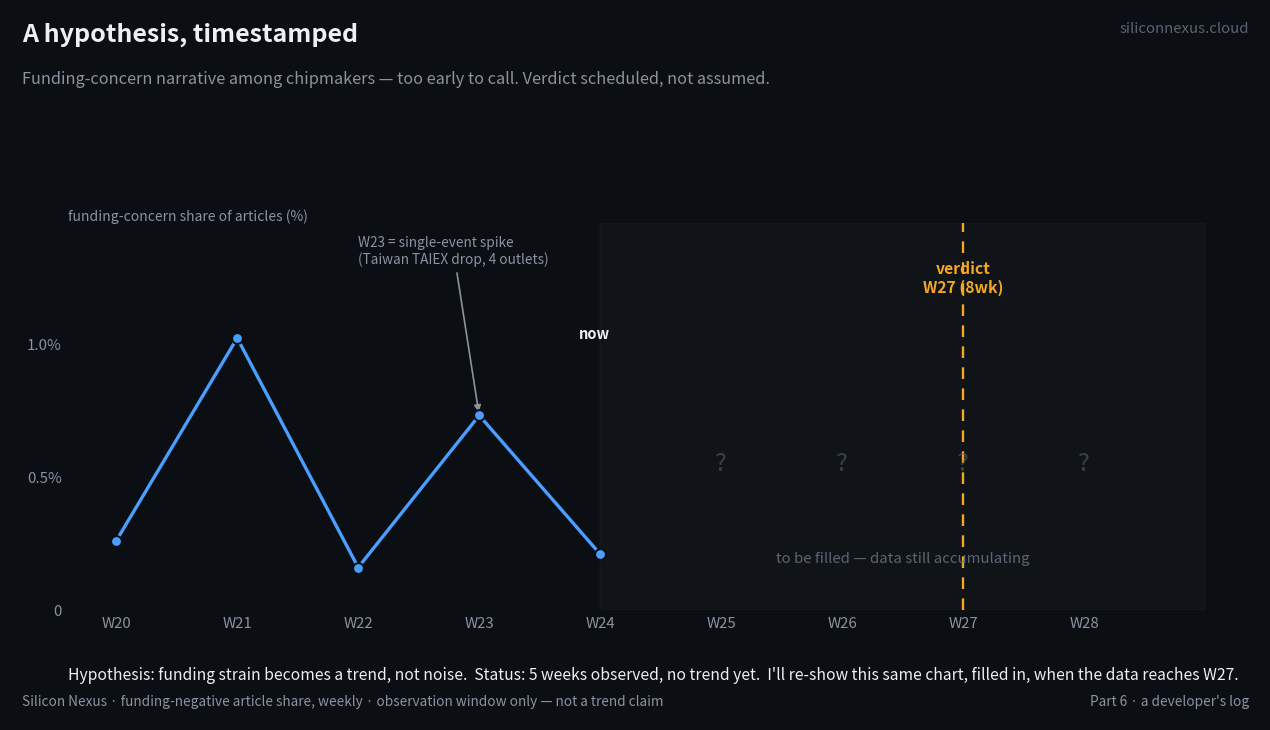

I went looking for whether the funding side is showing strain — not in the numbers yet, but in the narrative, by tracking how often chipmaker coverage turns to debt, leverage, and bond-market stress. Five weeks in, here's exactly what I have, no more:

That's not a trend. It's five noisy weeks, and the one visible spike is a single event — a Taiwan market drop covered by four outlets at once — not a signal. Phrases like "leverage strain" and "bond-market strain" have started appearing where the coverage used to be all order wins and record results, which is the kind of thing I want to watch. But five weeks tells you nothing you can trust.

So I'm doing something deliberate with that chart: I'm publishing it unfinished. The hypothesis is stated, the verdict date is set — week 27, early July, when there's enough data to actually judge — and the future is left blank on purpose. In a later column I'll show you this same chart, filled in, and we'll find out together whether the strain was real or noise. If I'm wrong, the chart will say so plainly.

Where that leaves it

So, plainly, and provisionally: everyone is building — the capex is real and at a record — but the shortage isn't easing, because the spending is being absorbed by HBM, the new fabs are years away, some supply is held back by choice, and the chips now face a power-and-permitting wall that money alone doesn't clear. The loop that's supposed to fix the memory cycle has its last link — spend becomes supply — stretched, delayed, maybe broken for this cycle.

That's my read today. I'd stress today. The AI buildout has only ever run in one direction, and four or five years isn't enough history to be sure of anything. Maybe the 2027 fabs arrive and the loop closes right on time and this column looks alarmist in hindsight. Maybe the power wall hardens and it looks, in hindsight, like the early sign of something bigger. I don't know which. What I can do is mark where I stood, timestamp the open questions, and come back to check the work when the data has had time to speak.

This is opinion, not investment advice — and explicitly the opinion of a developer who follows this market, not a financial professional. Where I've used figures, they're from primary filings and trade statistics, fact-checked as of writing; where I've reasoned past the data, I've tried to say so. The interpretation, and whatever corrections come later, are mine.