The Bill Behind the Beat — Opinion | Silicon Nexus

✍ Opinion· Jun 11, 2026· Silicon Nexus J.H.· human_opinion

The Bill Behind the Beat

Oracle just had its best quarter in fifteen years, and the market sold it. The number that scared investors is the same number that should tell you where to look next.

Oracle posted the best quarter it has had in over fifteen years, and the stock fell.

Cloud infrastructure revenue nearly doubled. The order book — remaining performance obligations, the contracted work not yet delivered — swelled by $85 billion in a single quarter to a record $638 billion. By every line that usually moves a stock, this was a blowout. And after the close, the market sold it off.

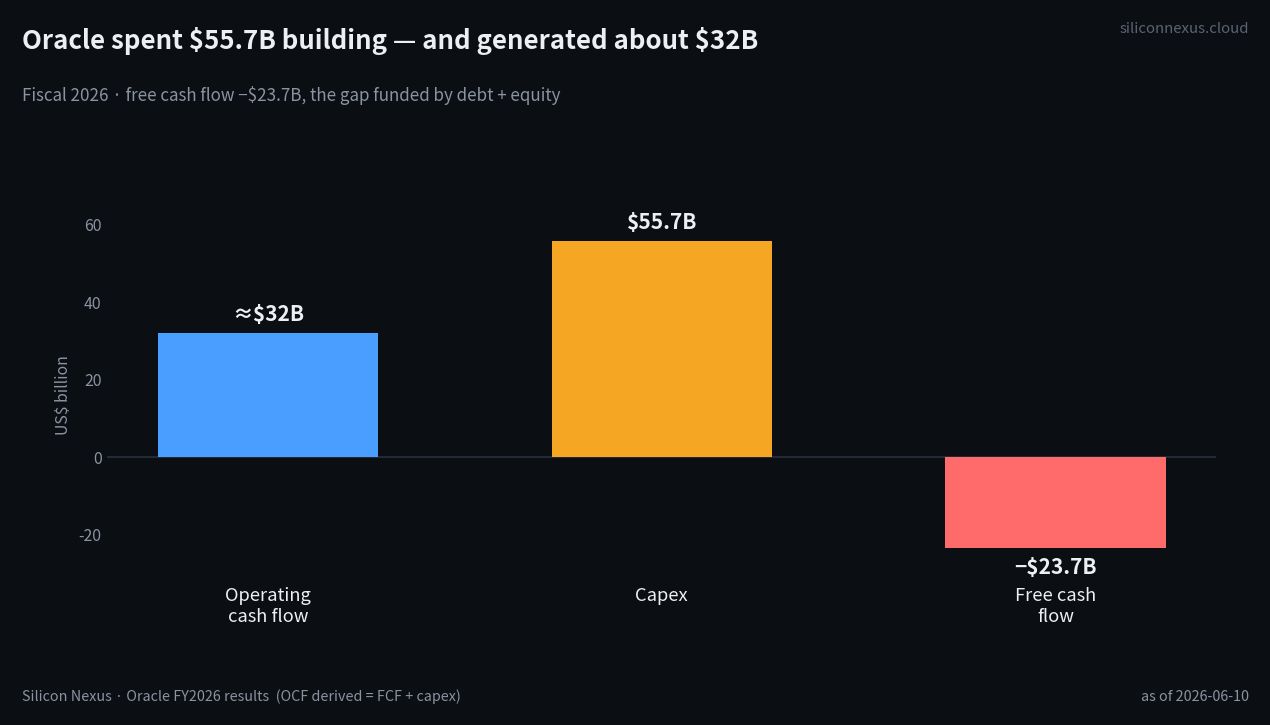

The reason was not the results. It was the bill. Oracle guided to roughly $70 billion of net capital spending for the year ahead, against the $55.7 billion it spent last year — itself already well above its own $50 billion guidance — and confirmed it will keep funding the build-out with a widening mix of debt and freshly issued equity. Record revenue, record backlog — and shareholders flinched at the cost of standing still.

That flinch is the subject of this column. Not because I think the AI build-out is about to break. Because I think most people are asking the wrong question about it.

The structural picture, not the single name

It would be easy to file Oracle under "one overextended company" and move on. The data says otherwise.

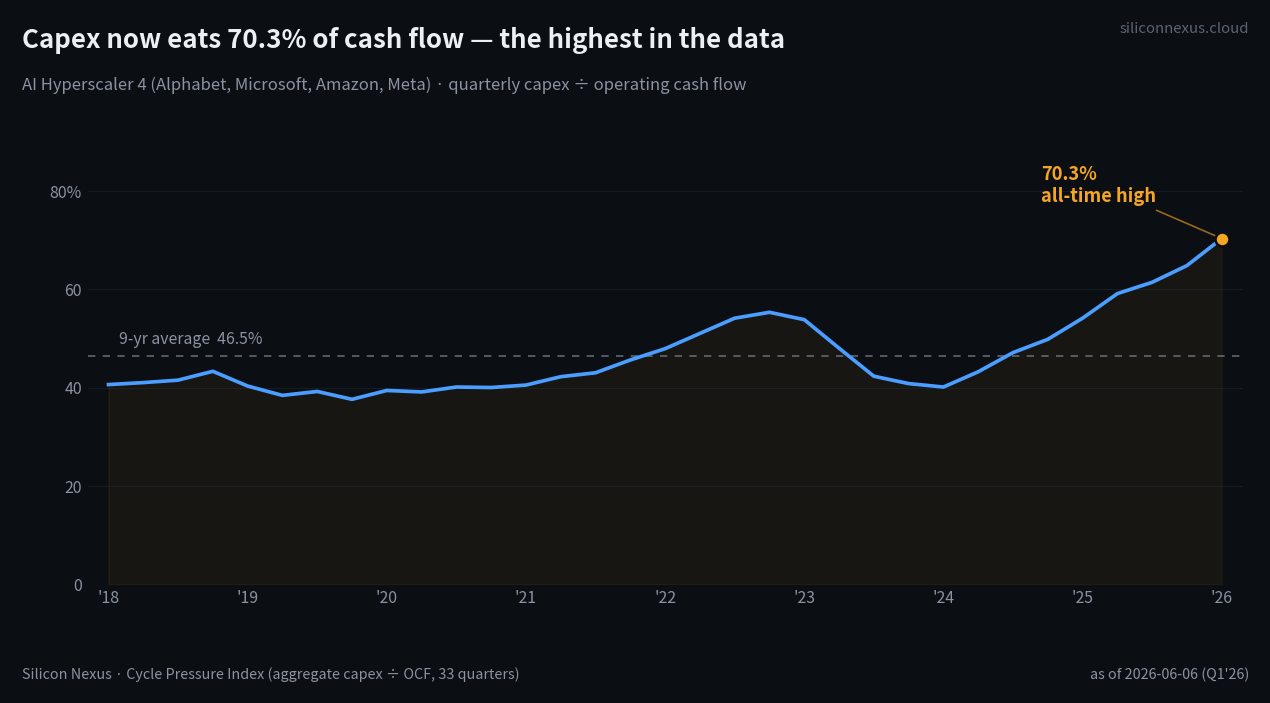

Across the four largest US hyperscalers, capital spending now runs at about 70% of operating cash flow — against a nine-year average closer to 46%. On our own Cycle Pressure Index, that reading sits at +30, the overheated band, and at the top of its 33-quarter history. This is not a single earnings call. It is the entire front edge of the industry spending cash faster than the business generates it, and then borrowing and issuing shares to cover the gap.

When a whole sector funds its growth this way, the textbook reaction is to call the top. Mark the cash-flow strain, point at the equity issuance, and wait for the correction. That is the cautious read, and on the numbers alone it is defensible.

I don't think it's right. Or rather — I think it's the right caution attached to the wrong model.

Why this doesn't stop on schedule

The standard model treats capex like a normal corporate decision: spend until the marginal return falls below the cost of capital, then stop. That model assumes the people writing the checks are optimizing returns. Increasingly, they aren't — or at least, that isn't the only thing they're optimizing.

Listen to how the buyers themselves frame it. Back at Alphabet's mid-2024 earnings call, pressed by analysts on when the AI spending would actually pay off, Sundar Pichai said the quiet part plainly: the risk of underinvesting is dramatically greater than the risk of overinvesting. That is not the language of return-on-capital. That is the language of a race you cannot afford to lose. (Notably, the same Pichai has more recently conceded to the BBC that the boom carries "elements of irrationality" and that no company — his own included — would be spared a sharp correction. Both things are true at once, and holding both is the whole point.)

Then look at the single largest expression of that mindset: Stargate. Announced from the White House in January 2025, standing next to the president, it is a pledge by OpenAI, SoftBank, and Oracle to deploy up to $500 billion over four years to build roughly 10 gigawatts of AI infrastructure on US soil — framed explicitly as securing American leadership in AI. Oracle is the builder. Its flagship Abilene campus already runs on Oracle Cloud Infrastructure, GB200 racks are being delivered, and a reported $300 billion, five-year cloud contract with OpenAI sits behind a large share of that $638 billion backlog. This is not a forecast of demand. It is contracted, politically blessed, and national in scale.

The state isn't only hosting the announcements, either. In August 2025 the US government took a roughly 10% equity stake in Intel — an $8.9 billion position, built largely by converting CHIPS Act grants into common stock. Strip away the politics and look at the motive: as NPR put it, this happened with no acute economic crisis and no war — the driver was competition with China and the race for AI. The government is now a shareholder in the domestic leading-edge logic base, and has openly said it wants more such deals.

When the largest buyers treat under-investment as the existential risk, and the government treats domestic compute and chipmaking as a national-security asset worth owning directly, capital expenditure stops behaving like a discretionary line item and starts behaving like defense spending: justified by the cost of not doing it.

Let me be careful here, because this is where I'm offering interpretation, not fact. The facts are the Intel stake, the capex figures, the quotes. The claim that this national-security framing keeps the spending going all the way to AGI is my read, not a proven trajectory. It could be wrong. But if it's even directionally right, then trying to time the end of the capex cycle is the wrong game entirely.

The question that actually matters

So drop the bubble-or-not question. It's binary, it's emotionally satisfying, and it's nearly impossible to answer in real time. Replace it with the question the spending itself raises: does the money earn?

On that question, the honest answer today is: not yet, not nearly enough — and that's exactly why the spending continues. The capital being deployed vastly exceeds the revenue it currently produces. But "returns haven't arrived" is not the same statement as "returns won't arrive," and the gap between those two is where every premature bubble call in technology history has died. There was, in hindsight, obvious over-investment in late-1990s internet infrastructure. There was also, in hindsight, no question that the internet was real. Both were true. The fiber got built, some of the builders went bankrupt, and the capacity got used.

That's the trap in calling the top: you can be completely right that it's overheated and completely wrong about what to do with that knowledge.

Follow the capital, not the cycle

Here is where I've landed, and it's deliberately unglamorous: don't predict when the capex stops. Watch where it flows, and watch the one gauge that tells you the flow is in trouble.

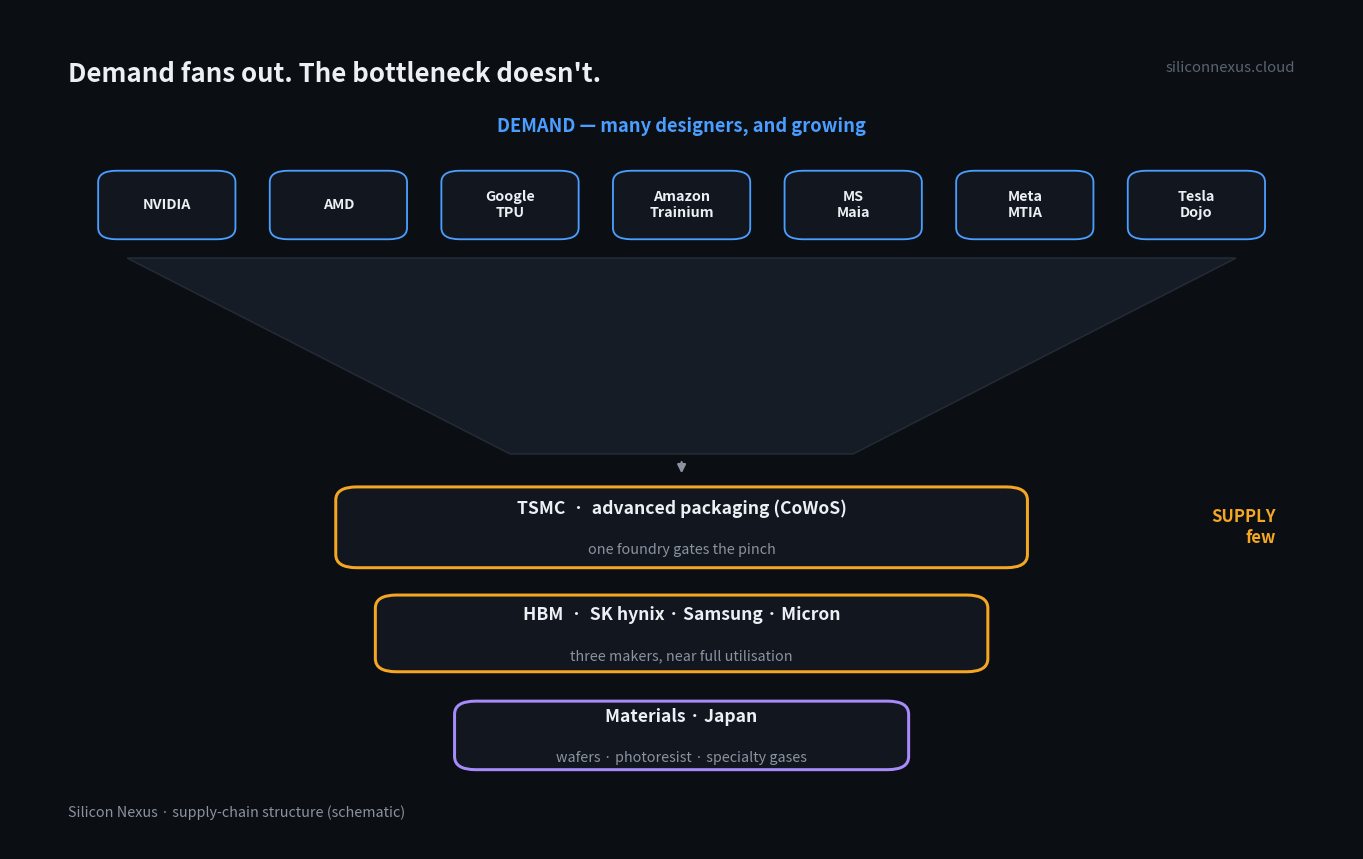

Where it flows is not evenly distributed. Oracle's $70 billion, Microsoft's, Meta's, Amazon's — that money funnels down a supply chain that narrows sharply. At the wide end, the spenders are many and getting more numerous. At the narrow end sit a handful of chokepoints: HBM made by three companies, advanced packaging gated by one foundry's CoWoS capacity, a short list of specialty materials and gases with single points of failure. Demand is broad; the bottleneck is narrow. That asymmetry — many buyers, few suppliers at the pinch — is the structural fact that survives whether or not the cycle "overheats."

So the bottleneck firms aren't where the bubble risk concentrates. They're where the contracted demand lands first and leaves last. Oracle's record $638 billion backlog is not an abstraction; it is future orders for compute that someone has to physically build, and the building runs straight through those chokepoints. You could hear it on Oracle's own call: management was pressed on memory and storage cost inflation and walked through how its contracts pass those rising costs through. The shortage I described last week is now a cost the buyers have to plan around — which is exactly what pricing power at a chokepoint looks like.

And the gauge? Free cash flow. Not the capex number — that won't stop, and watching it stop is watching the wrong thing. The number that matters is whether the cash flow underneath the spending stays healthy enough to carry it. Oracle just printed that number in its starkest form: free cash flow of negative $23.7 billion for fiscal 2026, the spending running years ahead of the cash it generates. When a buyer at that scale can fund the build-out from operations, the spending is self-sustaining. When it can't — when the funding shifts decisively to debt and dilution, as Oracle's negative free cash flow and fresh equity issuance now show — that's the signal worth tracking. And it cuts deeper than Oracle's own balance sheet: a large share of that record backlog rests on OpenAI, a customer that still loses billions a year and is itself leaning on debt to lease the chips it runs. The entity underwriting the build-out is not yet profitable. That doesn't make the demand fake — the racks are real and the contracts are signed — but it does make the funding chain, not the capex headline, the thing to watch. Not as a crash alarm. As the single macro vital sign for a thesis that is otherwise about plumbing, not timing.

What this changes for me

This is the conclusion, and it points at the next piece.

For a long time I tried to read this market the way the semiconductor industry has always been read — as a cycle, with one region or one stage leading another. I was wrong about that, and Part 5 is going to be about exactly how wrong, and what the data showed instead. The short version: what looked like a cycle was a four-to-five-year secular surge that began with the modern AI build-out, and the country-by-country lead-lag I expected to find wasn't there.

Part 4 is why that correction matters. If the capex won't be timed, and if the value concentrates at the chokepoints rather than rotating around a cycle, then the right unit of analysis was never the country and never the calendar. It's the node — the specific bottleneck where contracted demand collides with constrained supply — and the inventory and inter-firm orders that tell you how tight that node actually is.

Oracle's quarter was a beat with a bill attached. The market read the bill as a warning. I read it as a map. The capital is going somewhere specific. The job is to be standing where it lands — and to keep one eye on the cash flow that decides how long the flood lasts.

This is opinion, not investment advice. Figures are drawn from company filings and reporting and are fact-checked as of writing; interpretation is my own.