For three days the tape sold AI chips on glut fear. The same three days, the suppliers underneath printed record revenue — and rising prices. Here's the tell.

For three sessions in early June, the tape was ugly. The SOX fell 10.26% on June 5; Taiwan's TAIEX printed its largest-ever intraday point drop on June 8; and on June 9, US tech sold off again as Washington signaled fresh strikes on Iran. The word underneath the selling was glut — the fear that AI memory and components are tipping into oversupply.

But a glut has a signature, and this isn't it.

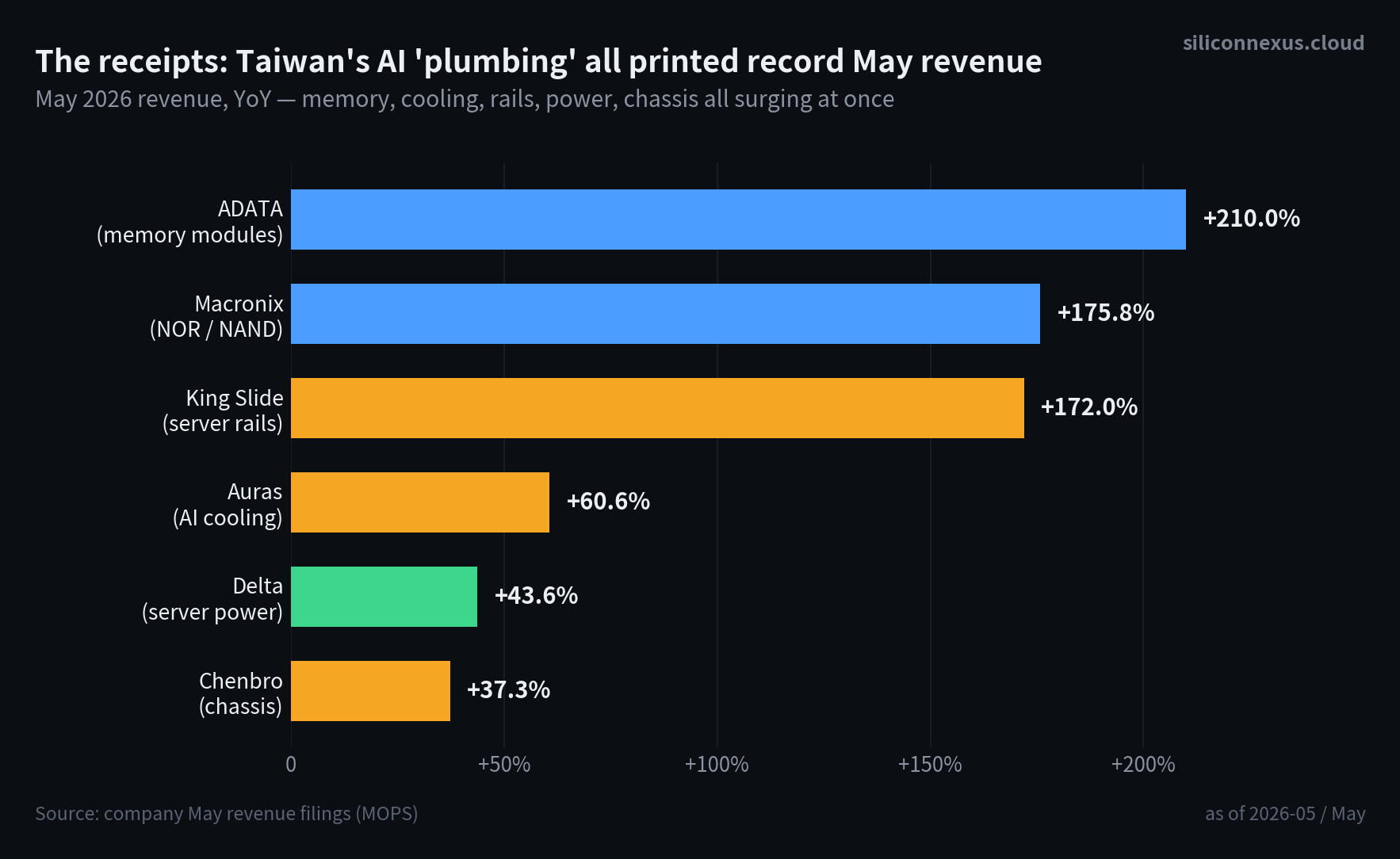

Look at the plumbing — the unglamorous layer beneath the GPUs and foundries, where AI infrastructure actually gets built. In May, Taiwan's suppliers printed records across every category at once: ADATA (memory) +210% YoY, Macronix (NOR/NAND) +176%, King Slide (server rails) +172%, Auras (AI cooling) +61%, Delta (server power) +44%, Chenbro (chassis) +37%. This isn't one hot product — it's the entire physical stack pulling at the same time. Delta, the largest, told investors plainly that capacity is still tight and material shortages are pushing costs up. Suppliers in a glut don't say that.

So is it just volume being shoved out the door — the kind of shipment surge that precedes a glut? No. Because price is moving the wrong way for that story.

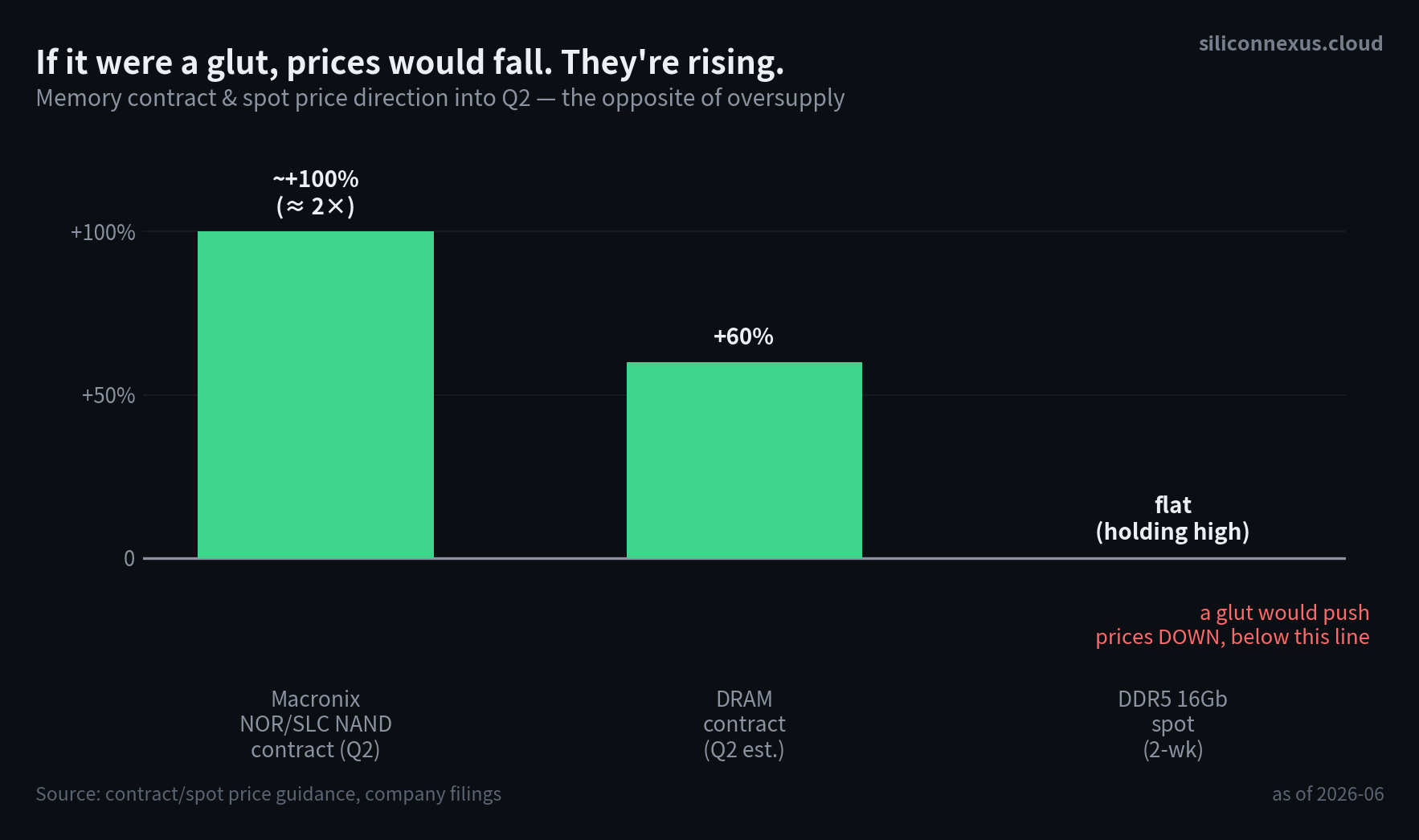

This is the tell. A glut means oversupply, and oversupply means falling prices. Instead prices are rising: Macronix guided NOR and SLC NAND contract prices up nearly 2× into Q2, DRAM contract prices are set to climb another ~58–63%, and DDR5 16Gb spot is holding at its highs. Volume and price are climbing together — that's the fingerprint of a shortage, not a glut. When supply genuinely outruns demand, price breaks first. It hasn't.

So why does the tape keep selling it as a glut? Because the market is pricing a future risk as if it were today's reality. The selloff was the discount rate, geopolitics, Korean leverage unwinding — and plain profit-taking after a sharp run, since these names had already surged through April and May. None of those touch what a memory module costs today. As for a real glut: it could come, but only when all this capex finally converts into supply a year or two out. That's a watchpoint, not a forecast. Until rising inventory days meet falling contract prices, a "glut" selloff is the tape arguing with its own receipts.

This is the same gap I've flagged all month: the receipts are real and the shortage is real — last week's 48-hour round trip already showed it was the tape that was wrong, not the fundamentals. So the supply question, to me, is settled for now. The one that isn't: who keeps funding the demand. That's where I'm looking next.

If this analysis was helpful · ☕ Support Us · ✈️ Telegram